Structural Cost Management: How to Achieve Cost Leadership

Verified

VerifiedCompanies are increasingly reassessing their internal cost structures, the value contributions of individual business units, and functional areas. A 2025 survey by BCG revealed that nearly 60% of companies had initiated cost-cutting and optimization strategies by late 2024.

This figure represented a 12-point increase from 2022, driven by inflation, energy volatility, and stagnating growth in major economies such as Germany and Japan. Corporate profits remain under pressure as real wage growth outpaces productivity in several sectors, forcing leadership teams to reevaluate their structural cost base.

The importance of structural cost transformation is increasing. Around 40% of CFOs surveyed by Deloitte in 2024 placed structural cost containment among their top three strategic priorities for 2025. Many of these efforts are aimed at enabling medium-term margin expansion while freeing cash for reinvestment or shareholder returns.

This article outlines the main steps to build a structural cost management approach, focusing on:

- Core focus areas: operational efficiency, cost optimization, and structural transformation

- Key success factors for preparing and executing cost management projects

- Strategic levers to reduce COGS, SG&A, and improve cash flow

By aligning cost management with strategy and execution, companies can reduce complexity and achieve a cost leadership positioning in their market.

Cost Structures Back in Focus

In 2025, cost management has returned as the top strategic priority for global executives, with one-third identifying it as their main focus, an 8 percentage point increase from the previous year.

According to BCG’s survey of over 570 C-suite leaders, only 48% of cost-saving targets were met in 2024, and companies that failed to meet these targets underperformed on total shareholder return (TSR) by an average of 9 percentage points compared to peers.

Many companies are now targeting structural improvements such as supply chain optimization and product portfolio simplification. Firms with cost-aware cultures and transparent leadership achieve up to 11% more efficient production processes.

Thus, low costs enable companies to achieve cost leadership or cost competitiveness within their sectors, free up resources for innovation and future investments, and outperform their competitors. McKinsey analyses show that companies with above-average total returns focus on revenue growth and consistently on cost management, regardless of the economic cycle!

Focus Areas in Cost Transformation and Cost Management

Cost transformation projects can vary greatly depending on the company, the business areas involved, and the intensity and complexity of the transformation.

Operational Optimization

Operational optimization projects are typically managed internally, using methodologies like Lean or Continuous Improvement (CIP). Companies that implement standardized Lean practices often achieve higher revenue growth and total shareholder returns compared to their peers.

Success in this area depends heavily on internal expertise and the ability to identify and improve inefficient processes. However, integrating external insights and proven best practices from other industries can significantly enhance outcomes.

Cost Optimization

Cost optimization efforts are often initiated internally but increasingly involve external cost efficiency consultants to accelerate execution and expand impact. These projects usually focus on cost avoidance and target areas where savings can be achieved quickly and with minimal disruption.

The success of these initiatives relies strongly on the second level of management, which is responsible for translating high-level goals into actionable measures and ensuring consistent implementation.

Structural Cost Transformation

Structural cost transformation projects are generally large in scope and require external support due to their complexity. These initiatives demand detailed planning, cross-functional coordination, and a formal project structure.

They offer the greatest potential for impact, delivering value over the short, medium, and long term. Structural transformations are often holistic, involving cultural change components that strengthen the broader organization and help embed cost discipline across all levels.

How Should a Cost Transformation Project Be Prepared?

1. Identifying the Success Factors

To lead a cost transformation successfully, a few key factors must be in place. One common issue is a drop in commitment from management, which often negatively affects other leadership layers and, ultimately, the project’s success.

Here are the key success factors:

- Full commitment from the management team, with clear and consistent communication

- Initiative framework aligned with company strategy and business model (internally & externally)

- Approach accepted and supported by the executive and leadership teams

- Goals that are realistic and tailored to the company

- A clear, practical plan with strong execution

- Balance between sustainable cost reduction and seizing growth opportunities

- Agile methods (80/20 rule) to quickly validate or discard hypotheses, optimizing cost-benefit outcomes

- Cultural alignment that promotes transparency, accountability, and incentivized behavioral change

- An independent implementation partner who not only helps design measures but also takes responsibility for implementation

2. Developing a Shared Vision with Stakeholders

As mentioned, management commitment is the most critical success factor for a cost transformation. Often, owners, management, and extended leadership teams have differing views on goals, ambition levels, and the urgency of the situation. These differences must be addressed at the outset of the project to develop a shared understanding: a vision.

With proper moderation, the company’s current operating model and functional blocks can be examined for their current and future value contributions.

3. Aligning Strategy and Shared Target Vision

A high percentage of transformations fail to achieve their goals, studies cite failure rates of 50–70%. Successful transformation and optimization require a unified approach and a shared vision coordinated with the leadership team.

Recommendation: Explicitly solicit, align, and consistently communicate target visions. Use moderated workshops to make implicit stakeholder goals explicit. For example, ask: “In this area, should performance be expanded (‘invested in’) or reduced (‘cut’)?”

Below, a framework you can use to align strategic goals with operational decisions across business functions. The visual illustrates how different departments are evaluated in terms of whether to invest (expand resources or capabilities) or divest (reduce or streamline activities) based on the company’s target vision.

- FTE (Full-Time Equivalent) indicates the number of full-time staff or equivalent workforce in a given function.

- Divest represents a planned reduction in resources (e.g., budget, headcount, activity).

- Invest represents a planned increase or focus on growth, capacity building, or strategic enhancement in that area.

Use this model to facilitate transparent discussions within leadership teams, enabling a shared understanding of where to allocate or withdraw resources in support of transformation objectives.

Project Execution – Creating Cost Transparency

The transparency phase requires detailed cost data to build business cases and compare scenarios. Controlling provides financial data such as cost centers, budgets, and actual spend. HR supplies personnel data (headcounts, salary structures, and workforce allocation) essential for analyzing labor costs, which often represent the largest expense category. Early access to both sets of data enables faster, more accurate decision-making during the planning phase.

Recommendation: Achieve financial transparency as early as possible. External consultants with the necessary know-how and experience can enhance efficiency and speed. To simplify, data can be broadly divided into personnel-driven and material costs. Further details can be added based on data availability, such as spend cubes for material costs.

Evaluating Value Creation Areas

Next, the value contribution of each company function is assessed, primarily through qualitative management interviews. This helps business units understand each other’s needs and improves interdepartmental collaboration. Results form the basis for optimizing service portfolios of business units and functions.

There are different models for how corporate headquarters maximize their value contribution and, consequently, the overall company value. Three overarching levers include:

- Shaping the future through innovation and coordination of the corporate network

- Unlocking performance via cross-unit resource management, performance improvements, and shared services

- Safeguarding the company group through governance and risk management

Optimization Levers for Generating Measures

After the top-down definition of the target corridor by management, the focus area or scope must be defined. Numerous levers can optimize structural costs. Obviously, project complexity increases with the number of parallel value levers and measures.

Recommendation: Maintain a clear focus on dimensions and selected levers. Depending on the company’s situation and transformation goals, the appropriate levers should be chosen. Experience shows that a sharper focus leads to more suitable measures and more effective cost savings.

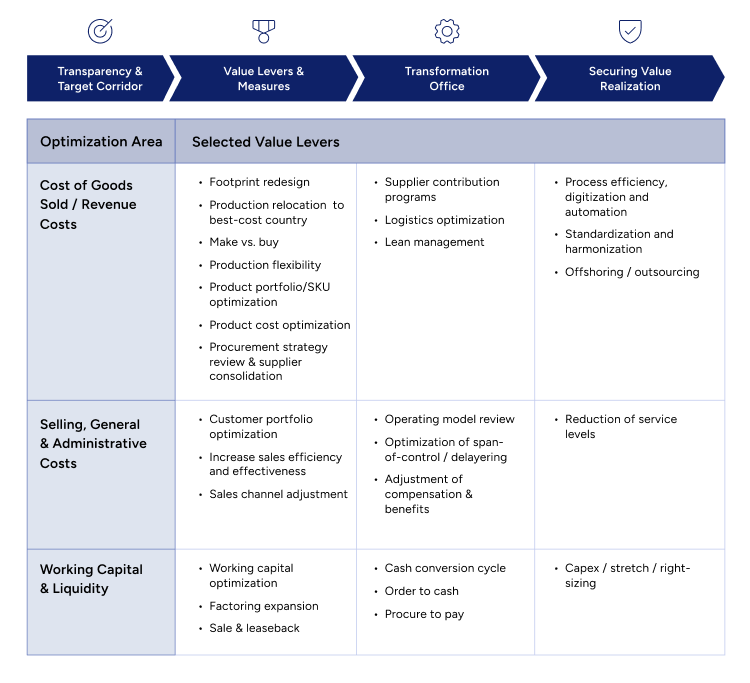

Strategic Cost Management Levers Across P&L Drivers

The following framework categorizes strategic optimization levers across key P&L cost areas, helping guide focused transformation efforts and value realization initiatives.

1. Cost of Goods Sold (COGS – Manufacturing/Material Costs)

Reducing COGS and improving gross margin can be achieved through product portfolio optimization, footprint adjustments, and production efficiency gains. Effects can be grouped using a severity logic. Portfolio optimizations and automation measures often show quick potential and can be quantified theoretically, but require coordinated execution and experience.

2. Selling, General and Administrative Costs (SG&A)

Some sales-related costs can be cut more quickly, delivering rapid effects in challenging business environments. Streamlining service portfolios and adjusting service levels can reduce personnel costs. Procurement optimization (e.g., renegotiation, supplier consolidation) is now a standard lever. The biggest effects come from redesigning operating models and reducing organizational complexity, including changes to span of control and decision-making agility.

3. Cash & Liquidity

Properly managed, these are central to increasing enterprise value. Balancing delivery capabilities and inventory levels can be optimized through governance, parameter settings, and AI-supported tools. Efficient cash conversion cycles improve liquidity and reduce refinancing costs in the medium term.

Measure Development

Measures should be developed bottom-up with functional leaders to ensure feasibility and commitment.

Recommendation: Measures should be presented to management for evaluation, aligned with company strategy, including savings potential, implementation effort, and risks. Also include implications, such as discontinued administrative services or limitations in sales support.

A countercurrent approach (top-down targets, bottom-up development, and management-level decision-making) enables structured alignment with strategy and encourages leadership-level buy-in. This is critical for achieving the desired effects. If cost reduction targets are missed, companies often have to launch new programs, this can be avoided with the right approach.

How to Maximize Implementation Success

Establishing a Transformation Office

Most companies don’t have a knowledge problem—they have an execution problem. A dedicated Transformation Management Office (TMO) working alongside the management team helps ensure implementation success and effect realization.

Recommendation: Sustainability comes from sustained effort—do it with the right team! Using tools beyond Excel can quickly provide transparency around current status, risks, and deviations. However, “A fool with a tool is still a fool.”

Tools are only part of the solution. Sustainable implementation also requires cross-functional collaboration, consistent follow-up, networking, and communication. After rollout, the overall situation and market conditions must be regularly reviewed. Adapting goals and responding flexibly is essential to balancing cost savings and market opportunities.

Change Management as a Differentiating Factor

Effective stakeholder management through tailored communication remains underestimated. Customized change management aligns with corporate culture and helps anticipate and overcome resistance, building acceptance and engagement.

Recommendation: Everyone talks about change management—the right communication fits the culture, conveys relevant information, and strikes the right, binding tone. Clear, honest communication and consistency in messaging are crucial to explain the change, share the vision, and clarify the reasons behind it. A clear timeline for the upcoming transformation must also be communicated.

Cost Management at Consultport

To drive a successful cost management project, companies should focus on three critical areas: operational optimization, targeted cost reduction, and long-term structural change. As outlined in this article, first published in Controller Magazin, we explored the strategic levers available to reduce COGS, streamline SG&A expenses, and improve overall liquidity.

However, transformation programs still often fail. Around 70% fall short, often due to a lack of leadership commitment, resistance from within the organization, or slow execution. To address these problems, companies turn to independent consultants.

Cost reduction consultants help cut expenses by analyzing spend, fixing inefficiencies, renegotiating supplier contracts, and improving procurement and workflows, often at a lower cost than traditional firms. Platforms like Consultport match companies with vetted experts in 48 hours, speeding up hiring and reducing costs.

Need support? Find a consultant.

Verified

VerifiedPatric Ayasse is a transformation and restructuring expert with over 20 years of experience across 50+ projects. A former Senior Manager at Deloitte and Head of Operations at Horváth, he specializes in cost optimization, target operating models, and interim CFO roles. Patric has led transformations for Fortune 500 firms and private equity portfolio companies in industrials, logistics, chemicals, and finance. He is known for combining board-level advisory with hands-on execution to drive measurable business results.

on a weekly basis.